Knight Frank/Markit House Price Sentiment Index (HPSI) – January 2016

Key headlines for January 2016

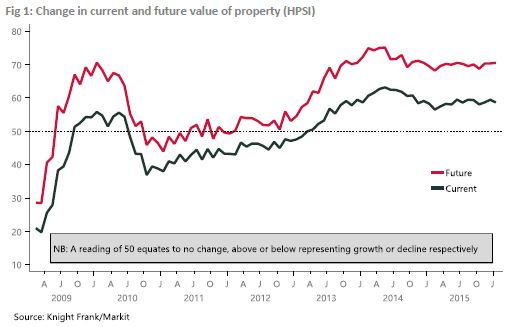

Change in current house prices

Households across the UK perceive that the value of their home rose in January, according to the House Price Sentiment Index (HPSI) from Knight Frank and Markit Economics.

Some 20.9% of the 1,500 households surveyed across the UK said that the value of their home had risen over the last month, while 3.6% said that prices had fallen. This resulted in a HPSI reading of 58.7 (see figure 1).

This is the thirty-fourth consecutive month that the reading has been above 50.

Any figure over 50 indicates that prices are rising, and the higher the figure, the stronger the increase. Any figure below 50 indicates that prices are falling.

January’s reading was a slight decrease from the 59.4 recorded in December, but returns the index to the same level as seen in November. It is just slightly higher the average reading of 58.5 recorded throughout 2015, but remains below the peak of 63.2 in May 2014, reflecting the easing in average UK house price growth seen since then.

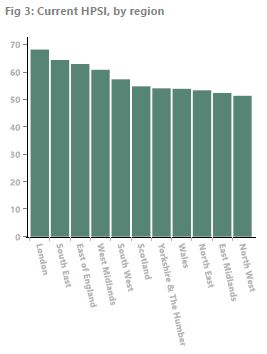

Households in all of the eleven regions covered by the index reported that prices rose in January, led by households in London (68.1) and the South East (64.3), although in both cases these sentiment index readings were slightly lower than in December.

The current sentiment index was lowest for the North West (51.3) and the East Midlands (52.3), indicating that households in these regions perceived the most modest rise in prices across the UK in January.

A lead indicator

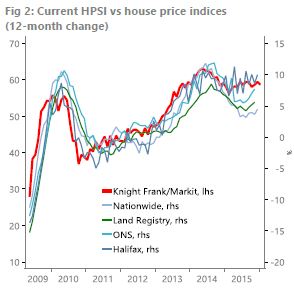

Since the inception of the HPSI, the index has been a clear lead indicator for house price trends. Figure 2 shows that the index moves ahead of mainstream house price indices, confirming the advantage of an opinion‐based survey which provides a current view on household sentiment, rather than historic evidence from transactions or mortgage market evidence.

Outlook for house prices

The future HPSI (figure 1), which measures what households think will happen to the value of their property over the next year, rose slightly in January (70.5) from December (70.3). This is the highest reading since June 2015, but remains below the peak of 75.1 reached in May 2014.

Households in the East of England chalked up a record high reading for future house prices expectations (81.1), indicating they anticipate the largest increase in the value of their home over the next 12 months, as shown in the tables on page 3. Londoners (79.1) continue to expect strong growth in prices over the next year, with the highest reading for the region since May 2014.

Meanwhile, there was a notable drop in the future reading for the North West (index down from 67.5 to 62.3 in January) as well as Scotland, which fell to 61.8, down from 65.8 in December, and an average reading of 65.1 throughout 2015.

Mortgage borrowers are the most confident that prices will rise over the next year (76.0), followed by those who own their home outright (73.1).

Gráinne Gilmore, head of UK residential research at Knight Frank, said:

“Households expect house prices to rise again in 2016. The future sentiment index is now sitting just above where it was in January 2015, and we now know that UK house prices climbed by 4.5% during the course of the year.

“The latest house price sentiment index suggests that monetary and political housing policies have not had a dramatic impact on households’ assessment and outlook for the value of their property.

“Mortgage borrowers are the most positive about the outlook for house prices over the next year, perhaps reflecting the anticipation of a longer period of ‘ultra-low’ rates after the Bank of England’s decision to hold rates this month, and signals from rate-setters that the UK base rate could be at 0.5% for some time yet.”

Tim Moore, senior economist at Markit, said:

“UK house price sentiment was little-changed overall at the start of 2016, with households across all regions continuing to anticipate rising property values over the course of the year. Historically, this index has been quick to signal upcoming changes in property market conditions. As a result, January’s strong survey figures suggest that UK house price sentiment has so far been resilient in the face of recent global financial market jitters and a more gloomy economic news flow.”

Knight Frank/Markit House Price Sentiment Index (HPSI) – Data Summary

Courtesy: Knight Frank and Markit

Knight Frank

Jamie Obertelli, PR Manager

+44 20 7861 1104

Gráinne Gilmore, Head of UK Residential Research

+44 20 7861 5102

+44 77 8552 7145

Oliver Knight, Senior Analyst

Markit

Joanna Vickers, Corporate Communications

Telephone: +44 20 7260 2234

Email: [email protected]

Tim Moore, Senior Economist

+44 14 9146 1067

+44 20 7861 5134

About the HPSI

The Knight Frank/Markit House Price Sentiment Index (HPSI) survey was first conducted in February 2009 and is compiled each month by Markit.

The survey is based on monthly responses from approximately 1,500 individuals in Great Britain, with data collected by Ipsos MORI from its panel of respondents aged 18-64. The survey sample is structured according to gender, region and age to ensure the survey results accurately reflect the true composition of the population. Results are also weighted to further improve representativeness.

Prior to September 2010, the Household Finance Index was jointly compiled by YouGov and Markit based on monthly responses from over 2,000 UK households, with data collected online by YouGovplc from its representative panel of respondents aged 18 and above. The panel was structured according to income, region and age to ensure the survey results accurately reflected the true composition of the UK population. Results were also weighted to further improve representativeness.

Index numbers

Index numbers are calculated from the percentages of respondents reporting an improvement, no change or decline. These indices vary between 0 and 100 with readings of exactly 50.0 signalling no change on the previous month. Readings above 50.0 signal an increase or improvement; readings below 50.0 signal a decline or deterioration.

IpsosMORI technical details (January survey)

IpsosMORI interviewed 1,500 adults aged 18-64 across Great Britain from its online panel of respondents. Interviews were conducted online between 13th and 17th January. A representative sample of adults was interviewed with quota controls set by gender, age and region and the resultant survey data weighted to the known GB profile of this audience by gender, age, region and household income. Ipsos MORI was responsible for the fieldwork and data collection only and not responsible for the analysis, reporting or interpretation of the survey results.

About Knight Frank

Knight Frank LLP is the leading independent global property consultancy. Headquartered in London, Knight Frank and its New York-based global partner, Newmark Knight Frank, operate from 244 offices, in 43 countries, across six continents. More than 6,840 professionals handle in excess of US$755 billion (£521 billion) worth of commercial, agricultural and residential real estate annually, advising clients ranging from individual owners and buyers to major developers, investors and corporate tenants. For further information about the Company, please visit www.knightfrank.com.

For the latest news, views and analysis on the world of prime property visit Knight Frank's new website Global Briefing at http://www.knightfrankblog.com/global-briefing/. And follow us on twitter @kfglobalbrief and @knightfrank.

About Markit

Markit is a leading global diversified provider of financial information services. We provide products that enhance transparency, reduce risk and improve operational efficiency. Our customers include banks, hedge funds, asset managers, central banks, regulators, auditors, fund administrators and insurance companies. Founded in 2003, we employ over 4,000 people in 11 countries. Markit shares are listed on Nasdaq under the symbol MRKT. For more information, please see www.markit.com.

The intellectual property rights to the HPSI provided herein is owned by Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without Markit’s prior consent. Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Markit and the Markit logo are registered trademarks of Markit Group Limited.

© 2005 - 2026 | Portfolio Property Investments | Powered by the PPI Business Platform