Analysing the impact of Currency movements on rime residential markets around the world

SUMMARY

CURRENCY MATTERS

In global prime property markets even small percentage changes in currency can have significant monetary implications.

Currency, ownership costs and taxation are becoming increasingly important considerations for investors, especially as the rate of price appreciation slows in some global city markets.

However, individuals need to be conscious of the risks, as well as the opportunities, surrounding these. The volatility observed in currency markets over the last 12 months is a case in point.

Does currency matter?

Fluctuations in currency markets can impact demand for residential property from international buyers.

To judge the strength of a country’s currency relative to its peers we have looked at effective exchange rates, rather than simply measuring one currency against another. This allows us to see in which direction a particular currency is moving in comparison to a weighted average of a basket of other major currencies.

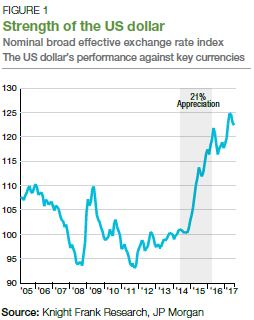

Between June 2014 and January 2016, the US dollar appreciated by 21%, making it more expensive for international buyers to purchase in the US. In recent years the strong US dollar, has had a notable influence on nonresident purchases in the US.

This link between currency and crossborder transactions is underlined by data from the National Association of Realtors in the US which shows that the appreciation in the US Dollar between 2014 and 2016 coincided with a 25% fall in non-resident property purchases across the US. Purchases by US residents increased by 10% over the same time period.

Such data needs to be viewed from two standpoints. Whilst appreciation can be costly, for those from abroad who already own an asset in the US a strengthening currency could be viewed as an opportunity to enhance returns by selling and repatriating capital.

Time to act

Investors may look to hold out for the most optimal time to buy or sell in an attempt to maximise purchasing power or potential returns. However this strategy can be risky.

The trading volume of the global forex market is estimated to be over 25 times that of global stock markets; this naturally leads to volatility and therefore carries risk when deciding whether the exchange rate has reached a peak or trough.

Interventions by Central Banks and policymakers in currency markets can devalue currencies.

The Swiss Franc’s pegging and depegging against the Euro is a case in point. From 2009 the Swiss National Bank (SNB) pegged the Franc to the Euro at CHF1.2/Euro. This resulted in the Franc depreciating by roughly 7% against the majority of currencies from its pre-peg low.

On 15th January 2015 the SNB depegged the currency without warning, causing the Franc to fall by 14.5% on the day. However, over the next two months the Franc recovered, falling by roughly 8% in comparison to the CHF1.20 peg; a stark reminder that waiting for the bottom of the market can be a high risk strategy.

To hedge against the impact of such devaluations buyers may look to invest in currencies which have a negative correlation to their local currency.

GLOBAL CURRENCY MONITOR

Knight Frank’s Global Currency Monitor calculates real investment returns for international investors by combining changes in prime prices with currency shifts.

Currency shifts in markets are underpinned by several factors, the most significant being economic fundamentals, political and geopolitical risks and future expectations. From a stuttering global economic recovery to elections and referendums, 2016 provided numerous events of influence.

Annual returns

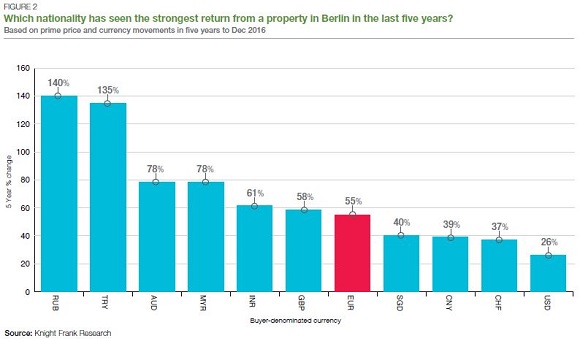

From the perspective of an investor looking to exit a market, British and Turkish homeowners abroad have seen the most significant returns over the last year, as a result of currency movements.

Sterling-denominated buyers who bought a prime property in Berlin in Q4 2015 and sold in Q4 2016 would have seen a 26% return and Turkish Lira-denominated buyers a 27% return. A Euro-denominated buyer would have realised a 9% return over the same time period.

Whilst currency shifts can be significant, it is important to keep in mind the fundamentals which underpin property markets, these can be the most significant drivers of performance.

Taking Berlin’s five year returns as an example, of the six currencies that have outperformed the local market over the last five years, all have experienced sudden political or economic upheaval. The imposition of sanctions on Russia and the recovery in the price of oil has influenced the Ruble. Uncertainty underpinned by political instability (Malaysia and Turkey) and referendums (Turkey and the UK) have led to depreciations in these countries’ currencies.

After these sharp depreciations, buyers denominated in these currencies have been subject to a material fall in their buying power. On the other hand, existing investors who are looking to repatriate their capital could use these deprecations as a method to enhance their returns.

The data digest on the back page provides additional city analysis on returns across key markets taking into account both currency and property market performance.

Opportunities

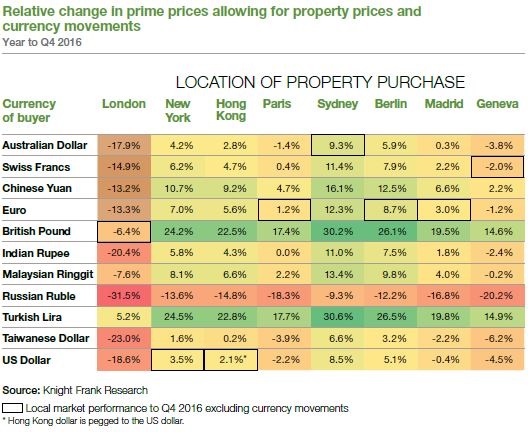

Below we have identified the key international buyers across six global cities and highlighted the extent to which currency shifts over the last year have influenced buying power. In our selected list of global cities, international buyers in London had the best opportunity for discounts on a currency basis alone between Q1 2016 and Q1 2017. A prominent example would be Ruble denominated buyers in London who in Q1 2017 would have found it 28% cheaper compared to Q1 2016. Over the same time period, Thai Bhat-denominated buyers in New York would have found their acquisition 9% cheaper if they had bought in March 2017 compared with March 2016.

OUTLOOK

Numerous factors can affect a currency’s performance, below we outline some of the key risks and their potential impact.

Risk Monitor

The Risk Monitor provides our latest assessment of key risks to global residential markets. Our risk score, out of a maximum of 10, is based on two assessments, firstly our view of the likelihood of the described scenario occurring, and secondly the potential market impact. Both these elements are scored from one (low) to five (high), collectively contributing to our combined Risk Score.

RISK: GLOBAL ECONOMIC GROWTH

SCENARIO: Slower than expected economic growth

IMPACT: Positive economic data from the US, Eurozone and Asia has surpassed expectations so far in 2017. However, there are several factors which will underpin the stability of this recovery. The pace of rate hikes, due to increasing inflationary pressure, may increase the cost of borrowing. Countercyclical fiscal policies could lead to a slowdown in employment and wages and influencing demand for prime residential property. This may slow lending, although higher rates may mean financial institutions are more willing to expand lending levels.

RISK: POLITICAL RISK

SCENARIO: French, UK and German National Elections

IMPACT: Populist movements across Europe are contributing to uncertainty on a national level and in the EU. However this threat has subsided given recent election results in the Netherlands and France. Any loss of medium-term confidence and divestment as investors look to de-risk, could impact on housing market activity. However, positive economic data in the EU and more stringent views on immigration by incumbent parties has reduced this risk to some degree and forced recoveries in currencies such as the Euro in recent times.

RISK: PROTECTIONISM

SCENARIO: Increased regulation of the property market and greater capital controls

IMPACT: In an effort to cool property markets policymakers have increasingly turned to regulation. The effectiveness of these regulations has always been a matter of debate; recently Vancouver and Singapore have softened previously introduced property regulations. Such political interventions in property markets can severely influence investment.

RISK: GEO-POLITICAL FACTORS

SCENARIO: Increased political instability in Russia, the Syrian crisis and North Korea

IMPACT: Global tensions have continued to develop since the start of the year. Russia’s growing involvement in Syria and North Korea’s increased military rhetoric are moving up investors’ agendas. These factors are important to global trade and resulting sanctions can have a knockon effect on trade routes, these could be detrimental to global economic growth and sentiment.

Ones to watch

What does a strong US dollar mean for global property markets?

Over the coming year, expansionary fiscal policy in the US is expected to bolster economic growth. The IMF forecasts growth in 2017 to reach 2.3%, up from 1.6% in 2016. Combined with expected interest rate hikes, this may lead to a stronger dollar.

For buyers denominated in US dollars this will mean an appreciation in buying power. However, emerging market denominated buyers may find their buying power weakened due to depreciating currencies. As the Federal Reserve enacts further hikes we may see other central banks following suit, increasing the cost of borrowing both in US dollar terms and in local markets. This could impact the demand for debt-funded property purchases.

International property investments and portfolio diversification are some of the most important investment decisions for ultra-high net worth individuals (UHNWIs) according to Knight Frank’s Attitudes Survey. Portfolio diversification ranks as one of the top five most important factors for UHNWIs. Over the next two years 32% of UHNWIs will look to invest in prime residential property outside of their country of residence. Whilst movements in currency markets can be important to overall returns it is important to consider these alongside fundamental market indicators such as price performance and yield, lacklustre performance here can offset shifts in the US dollar.

Courtesy: Knight Frank

DATA DIGEST

The table above shows relative change in prime prices allowing for property price and currency movements. The currency and price data is to Q4 2016, unless otherwise stated. From the perspective of an international investor currently look to purchase, a negative figure means purchasing prime property is cheaper compared to a year ago. For example an Australian buyer, denominated in Australian dollars, buying in Prime Central London would find it 17.9% cheaper in Q4 2016 compared to Q4 2015.

The global currency monitor is part of Knight Frank’s wider country and city level property database, for further information on this please contact Taimur Khan.

RESEARCH

Liam Bailey - Global Head of Research

+44 20 7861 5133

Taimur Khan - Senior Analyst

+44 20 7861 1436

PRESS OFFICE

Astrid Etchells

+44 20 7861 1182

Knight Frank Research provides strategic advice, consultancy services and forecasting to a wide range of clients worldwide including developers, investors, funding organisations, corporate institutions and the public sector. All our clients recognise the need for expert independent advice customised to their specific needs.

Important Notice

© Knight Frank LLP 2017 – This report is published for general information only and not to be relied upon in any way. Although high standards have been used in the preparation of the information, analysis, views and projections presented in this report, no responsibility or liability whatsoever can be accepted by Knight Frank LLP for any loss or damage resultant from any use of, reliance on or reference to the contents of this document. As a general report, this material does not necessarily represent the view of Knight Frank LLP in relation to particular properties or projects. Reproduction of this report in whole or in part is not allowed without prior written approval of Knight Frank LLP to the form and content within which it appears. Knight Frank LLP is a limited liability partnership registered in England with registered number OC305934. Our registered office is 55 Baker Street, London, W1U 8AN, where you may look at a list of members’ names.

© 2005 - 2026 | Portfolio Property Investments | Powered by the PPI Business Platform